Medicare Supplement Plan G vs Plan N in North Carolina

Table of Contents

If you're a North Carolina resident weighing Medigap Plan G against Plan N, the decision comes down to how much you want to pay upfront in premiums versus what you're willing to cover out of pocket. Both plans fill most of the gaps left by Original Medicare, but they do it differently.

Medicare Supplement plans (also called Medigap) pick up costs that Original Medicare doesn't, like coinsurance, copays, and deductibles. Plan G and Plan N are the two most popular options for North Carolina residents enrolling today, so here's how they compare.

"Depending on age, there are 10 to 12 Medicare Supplements to choose from, but there are really only two that people pick from: the Plan G and the Plan N. A very small percentage pick the High-Deductible G," says Chris Prang, a licensed Medicare agent in Virginia. That market reality is why this comparison matters for North Carolina residents: the real decision today is G versus N.

What Does Plan G Cover in North Carolina?

Plan G is the most popular Medigap plan on the market right now, and for good reason. It covers nearly everything Original Medicare leaves behind:

- Part A hospital deductible ($1,676 in 2026)

- Part A coinsurance and hospital costs up to an additional 365 days after Medicare benefits are used up

- Part B coinsurance or copayment (typically 20% of approved services)

- Part B excess charges (when doctors charge more than the Medicare-approved amount)

- First three pints of blood

- Skilled nursing facility coinsurance

- Foreign travel emergency care (80% of charges, up to plan limits)

The only gap Plan G leaves is the annual Part B deductible ($257 in 2026), which you pay once per year before Medicare Part B kicks in.

Because Plan G covers excess charges, North Carolina residents are protected if a doctor doesn't accept Medicare assignment. Excess charges can add up to 15% on top of your bill, so this protection matters if you see specialists who don't accept assignment.

One caveat on the foreign travel piece: the standard Medigap foreign travel benefit isn't as generous as it sounds. "There's a rider you can get if you have a Medigap or a supplement plan, a foreign travel rider. It's really not that good. There's a $250 deductible, the plan pays a $50,000 lifetime maximum benefit, and you're on the hook for 20% of the bill," says Mark Christiansen, a licensed Medicare agent in Wisconsin. If you travel internationally often, he recommends layering a separate travel medical policy on top, which he says typically runs around $200 for solid coverage on a one or two week trip.

What Does Plan N Cover in North Carolina?

Plan N covers most of the same benefits as Plan G, with a few notable exceptions. You still get coverage for the Part A deductible, Part A coinsurance, skilled nursing facility coinsurance, blood, Part B coinsurance, and foreign travel emergency care on the same terms as Plan G.

Here's where Plan N differs from Plan G:

- No coverage for Part B excess charges. If your doctor charges above the Medicare-approved amount, you pay the difference.

- Copays on certain visits. You'll pay up to $20 for office visits and up to $50 for emergency room visits that don't result in an inpatient admission.

The trade-off for these gaps is a lower monthly premium. For North Carolina residents who don't see non-participating doctors and rarely visit the ER without being admitted, those copays may never add up to much.

Plan N policyholders see the structure play out in everyday bills. "Because you're on a Medigap Plan N, Medicare pays first for a medically necessary procedure, and then your Plan N usually helps with most of what's left. You're still responsible for your Part B deductible each year, plus small copays for office and ER visits, and possibly Part B excess charges if your doctor doesn't take Medicare assignment," says Tamela Clayton, a licensed Medicare agent in Texas.

Side-by-Side Coverage Comparison

| Benefit | Plan G | Plan N |

|---|---|---|

| Part A Deductible | Covered | Covered |

| Part A Coinsurance and Hospital Costs | Covered | Covered |

| Part B Coinsurance | Covered | Covered, except for up to $20 office visit and up to $50 ER copays |

| Part B Deductible | Not covered | Not covered |

| Part B Excess Charges | Covered | Not covered |

| Skilled Nursing Facility Coinsurance | Covered | Covered |

| Foreign Travel Emergency Care | Covered (80% up to plan limits) | Covered (80% up to plan limits) |

| Blood (First 3 Pints) | Covered | Covered |

Both plans use the same foreign travel emergency structure: a $250 annual deductible, 80% coinsurance, and a $50,000 lifetime maximum. Plan N copays apply to office visits and to ER visits that do not result in inpatient admission.

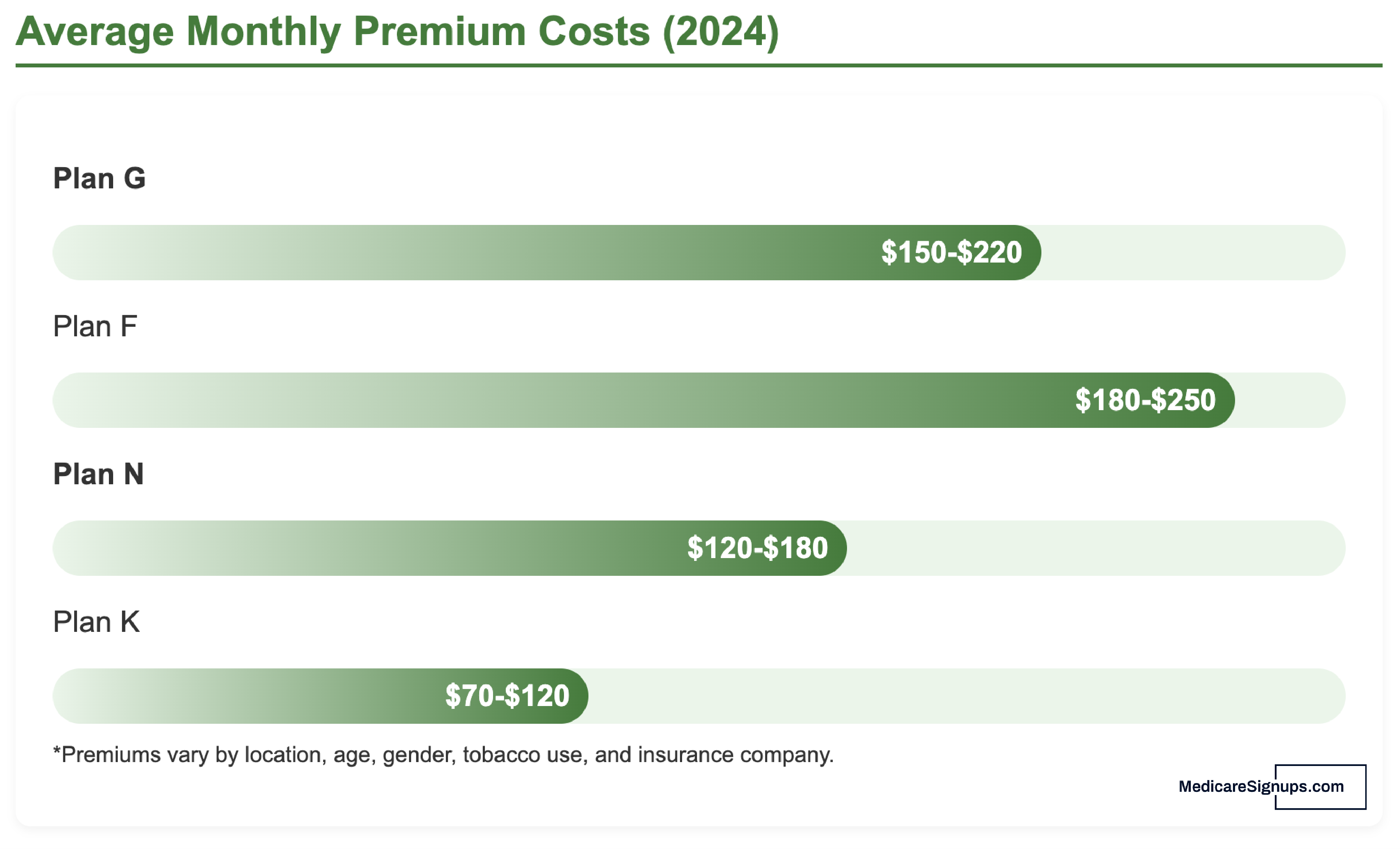

Plan G and Plan N Costs in North Carolina

Plan G premiums are higher than Plan N because you're buying more coverage. The exact difference depends on your age, location within North Carolina, gender, and the insurance carrier, but nationally, Plan G premiums tend to run $20 to $60 more per month than Plan N from the same carrier.

One thing to keep in mind when you're shopping NC carriers: the benefits themselves don't change. "Medicare Supplement plans like Plan G or Plan N are standardized by law. That means Plan G from Mutual of Omaha is the same as Plan G from Cigna; it just costs a little differently or has different customer service," says Randy Hill, a licensed Medicare agent in Ohio. Translation: shop on price, rate-increase history, and service, not on coverage details.

That said, premium isn't the whole picture. Plan N's lower monthly cost can be offset by the copays you'll pay at office visits and ER trips. If you visit your doctor frequently, those $20 copays add up. On the other hand, if you're generally healthy and rarely go to the doctor, Plan N's lower premium could save you hundreds per year.

How Medigap pricing works also matters here. Plans are priced using one of three methods: community-rated, issue-age-rated, or attained-age-rated. North Carolina may regulate which methods carriers can use, and the method affects how fast your premiums rise over time regardless of whether you pick G or N. Plan G prices can vary significantly from one NC zip code to the next.

When Plan G Makes More Sense

Plan G is typically the better choice if:

- You want the most predictable out-of-pocket costs possible

- You see specialists who may not accept Medicare assignment

- You want richer everyday coverage without office or ER copays

- You'd rather pay a higher premium than deal with copays at every visit

- You have chronic conditions that require frequent doctor visits

For North Carolina residents who value simplicity, Plan G is about as close to "pay your premium and forget about it" as Medigap gets. The only annual cost you'll pay beyond the premium is the Part B deductible.

When Plan N Makes More Sense

Plan N may be the smarter pick if:

- You're healthy and don't visit the doctor often

- All your North Carolina doctors accept Medicare assignment (most do)

- You rarely have ER visits that don't turn into admissions

- You prefer a lower monthly premium and can handle small copays

- You want to save money now and can always switch carriers later

The $20 office visit copay is a ceiling, not a flat fee. Some Plan N policyholders pay less than $20, and some visits (like preventive services covered by Medicare) don't trigger a copay at all since Medicare covers them at 100%.

If international travel is a factor, Plan N does cover foreign travel emergencies on the same terms as Plan G, so that piece shouldn't push North Carolina residents one direction or the other.

The Real Difference Between Plan G and Plan N for North Carolina Residents

Start by estimating your annual healthcare usage. If you see your doctor 12 times a year, that's up to $240 in copays with Plan N. Compare that to the annual premium difference between the two plans from NC carriers. If Plan G only costs $30 more per month ($360/year), and you'd spend $240+ in copays with Plan N, the math favors Plan G.

Use a step-by-step financial checklist to map out these numbers for your situation. Factor in not just premiums and copays, but also whether you value the peace of mind of excess charge protection.

Also consider when you're enrolling. During your Medigap Open Enrollment Period (the six months after you turn 65 and enroll in Part B), you have guaranteed-issue rights. Carriers can't charge you more or deny you based on health conditions. This is the best time to lock in either plan. If you're still working and have employer coverage, read about how Medicare coordinates with employer plans before making a decision.

That window matters because the door narrows fast. "If you start out with a Medicare Advantage plan and later down the line want to switch to a supplement plan years later, you'll be subject to medical underwriting, which puts you at risk of being declined for pre-existing conditions," says Justin Sonon, a licensed Medicare agent in Pennsylvania. For North Carolina residents, picking G or N during your initial enrollment window is the cleanest path to guaranteed coverage.

If you're not sure which plan fits your situation, working with a local Medicare agent in North Carolina can help you compare real quotes from carriers in your area. There's no cost to you since agents are paid by the insurance companies. They can also help you avoid common enrollment mistakes that first-time Medicare enrollees often make.

Eligibility for Plan G and Plan N in North Carolina

Both plans require enrollment in Original Medicare (Parts A and B). If you're enrolled in a Medicare Advantage plan, you'll need to switch back to Original Medicare before you can buy a Medigap policy.

You must also be at least 65 in most states, though North Carolina may offer Medigap access for people under 65 who qualify for Medicare due to disability. Check Medicare Supplement eligibility requirements to confirm you qualify and review the Medicare Supplement FAQ for answers to other common questions. Be mindful of Medicare penalties if you delay enrollment past your initial window.

Johnny Baldino

Licensed North Carolina Medicare Agent

Contact Johnny through Medicare Agents Hub »

Hey there, my name is Johnny, and I am your local Medicare advisor and broker. I specialize in all things Medicare, Life insurance and final expense insurance and am devoted to helping you find the best plan that matches your specific needs and financial situation. I will take care of the daunting task of comparing plans from well-known national and local companies for you. Even better, my services are completely free! I know that sounds crazy but its true, I am paid by the carriers and I take of you for free. Contact me today to explore your Medicare options, and be sure to mention that you found me on Medicare Agents Hub!

Matt Feret

Author, Prepare for Medicare - The Insider’s Guide

https://prepareformedicare.com

Matt Feret is the author of the Prepare for Social Security - The Insider’s Guide and the Prepare for Medicare - The Insider’s Guide book series and launched PrepareforSocialSecurity.com to help people get objective answers to questions about Social Security and Medicare. Matt is also the host of The Matt Feret Show. He has held leadership roles at numerous Fortune 500 Medicare health insurers in sales, marketing, operations, product development, and strategy for over two decades.